The Relationship and Impact of the External Auditor’s Feeson Audit Quality of Financial Statements: A Case Study on Audit Companies and Offices Operating in Iraq

DOI:

https://doi.org/10.51173/tjms.v2i1.25Keywords:

auditor’s fees, audit quality of data, accounting information, International standards on AuditingAbstract

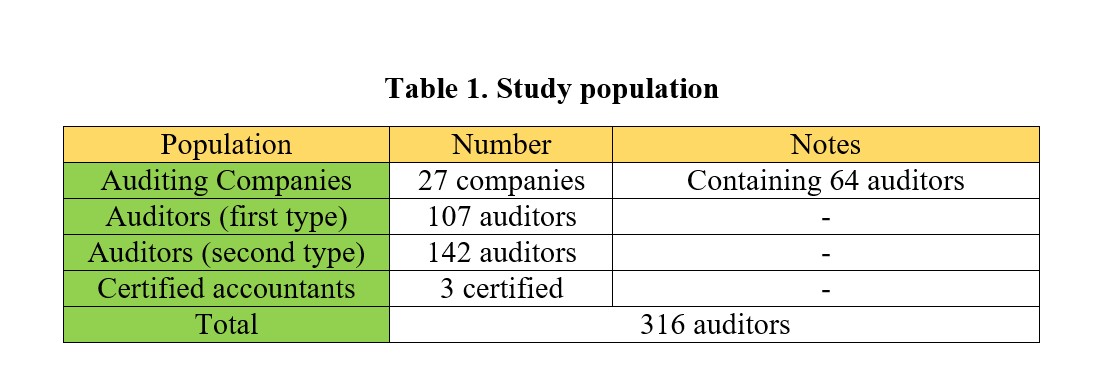

The aim of this study is to indicate the impact of the auditor's fees (audit tenure, size of the audited company, complexity level of the company, risk faced by the company) on audit quality. According to the Auditors’ Bulletin published by the Iraqi Board of Controlling and Account auditing, the study population include 316 working audit offices in Iraq. The questionnaires were distributed to the study sample (N= 225) of the workers in the research organization using the method of random samples. Then, the (225) questionnaires were analyzed by the statistical program (SPSS). International Standards on Auditing for the significance level (α ≤ 0.05) in the Iraqi business environment. The study concluded that the auditor’s fees related to companies or auditing institutions have a statistically significant effect (α 0.05) on the quality of the company auditing statements and accounting information in the Iraqi business environment, based on the International Standards on Auditing.

References

R. Saadawi and A. N. Touarehi, “Factors affecting the quality of external audit from the perspective of auditors in Algeria,” M.S. thesis, Mohamed Boudiaf University, Al-Messila, Algeria, 2021.

M. Al-Amin, “Factors affecting audit fees of the external auditor and how to determine them: A field study in the Syrian environment,” Tishreen University Journal, vol. 39, no. 2, 2017.

S. Abdel-Alim Najati, “The Impact of Dual and Joint Audit on Audit Risks,” 2020.

Saud et al., “Determinants of Audit Quality and its Impact on the Performance of the External Auditor: a pilot study of the opinions of a sample of external audit offices and companies,” 2020.

H. Dahdouh and A. Ramadan, “The Effect of the Auditor’s Fees on Audit Quality Process: A Field Study in the Audit Offices Operating in Damascus,” Journal of Hama University, vol. 2, no. 4, 2019.

S. Al-Naasan, “Factors affecting the audit quality from the perspective of external auditors,” M.S. thesis, Islamic University, Gaza, 2018.

M. Nammour, “The effect of Auditors’ Fees on Audit Quality Process in Syria,” M.S. thesis, Syria, 2017.

Z. F. Dewi, “The Effect of Audit ethics, UDIT, Audit fees, Auditor Experience and Competence on Audit Quality in The Public Accounting Firm (KAP) Padang City,” Journal Point Equilibrium Manajemen & Akuntansi, vol. 3, no. 1, pp. 98–116, 2021.

M. Ziad and A. Safaa, “Determinants of Audit Fees and the Role of the Board of Directors and Ownership Structure: Evidence from Jordan,” The Journal of Asian Finance, Economics and Business, vol. 8, no. 5, 2021.

M. Hussein and M. Alshammary, “The Extent to which Auditors Apperception their Responsibilities in the Importance of Implementing the Economic Units of Transparency Indicators and their Reflection on the Quality of the Audit Process,” Journal of University of Babylon for Pure and Applied Sciences, vol. 27, no. 6, 2019.

O. Jushua, “Audit Fees and Audit Quality: A Study of Listed Companies in the Downstream Sector of Nigerian Petroleum Industry,” Journal of Business Economics (JBE), vol. 85, no. 1, 2018.

E. K. Kilmili, “Determinants of Audit Fees Pricing: Evidence from Nairobi Securities Exchange (NSE),” International Journal of Research in Business Studies and Management, vol. 3, no. 1, 2016.

R. A. Z. Al-Shuhnah, Auditing: A contemporary approach according to International Standards on Auditing (Theoretical Framework), 1st ed., Jordan: Dar Wael for Publishing and Distribution, 2015.

H. A. Mohammad and W. K. Nagres, “Integrating internal and external auditing and its impact on the quality of reports of external auditors,” University of Kirkuk Journal for Administrative and Economic Science, vol. 10, no. 2, 2020.

E. J. Aronmwan and C. A. Okafor, “Auditee characteristics and audit fees: An analysis of Nigerian quoted companies,” Journal of Social and Management Sciences, vol. 10, no. 2, pp. 68–79, 2015.

G. S. Abu Hudaib, “Determinants of external audit fees in Jordan: An applied study on service companies listed on the Amman Stock Exchange,” M.S. thesis, Jordan, 2017.

J. I. Saliha and H. H. Flayyihb, “Impact of audit quality in reducing external audit profession risks,” International Journal of Innovation, Creativity and Change, vol. 13, no. 7, pp. 176–197, 2020.

S. N. Yassin, “The Role of Joint Auditing in Improving the Quality of the Auditor’s Report - A Field Research on a Sample of Auditing Offices in Iraq,” Arab Institute for Certified Public Accountants, 2021.

Chakrabarty, S. Duellman, and M. A. Hyman, “A new approach to estimating the relation between audit fees and financial misconduct,” Accounting Horizons, vol. 34, no. 2, pp. 41–61, 2020.

M. M. Ali, “The relationship between the comparability of financial statements and audit fees: The modified role of the auditor’s and his client’s characteristics,” Alexandria Journal of Accounting Research, vol. 6, no. 1, 2022.