The Effect of the Source of Commitment and Ethical Style of Auditors on Independent Auditors’ Whistle-blowing

DOI:

https://doi.org/10.51173/tjms.v1i1.8Keywords:

Source of Commitment, Ethical Style, Auditors’ Whistle-blowingAbstract

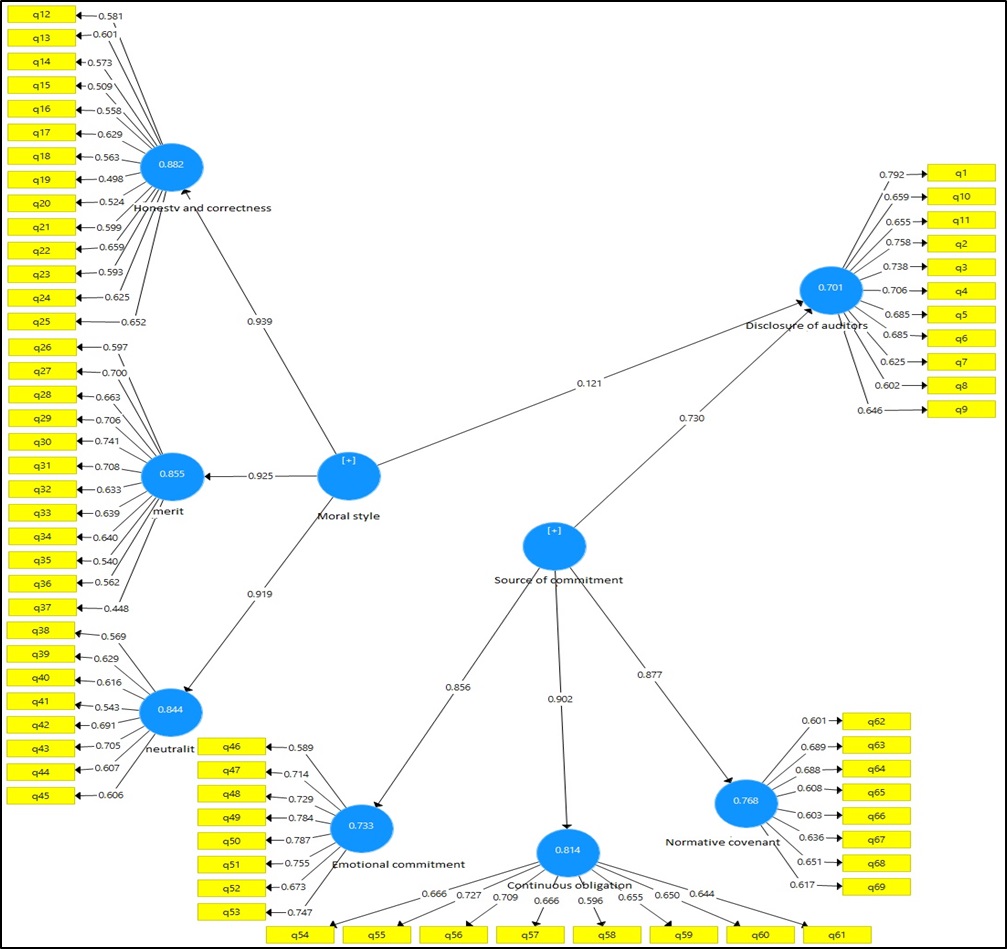

Purpose: The present study was conducted with the aim of investigating the effect of the source of commitment and ethical style of auditors on disclosure (whistle-blowing) of independent auditors.Method: The current study was carried out utilizing a descriptive correlational methodology. The statistical population of the present study was made up of 248 independent auditors. The instrument used in the present study was the standard questionnaire of Maragno and Cordero (2022) (includes disclosure of auditors with 11 items, source of commitment with 24 items, and ethical style with 34 items) whose face validity was confirmed by a number of respondents and reliability. They were also estimated using Cronbach's alpha coefficient for auditors' expressiveness of 0.888, ethical style of 0.915 and source of commitment of 0.848. Structural equation modeling was used to analyze the research data.Research findings: The results of the research hypotheses test showed that the source of commitment to the organization (emotional commitment, continuous commitment and normative commitment) has a positive effect on the disclosure (whistleb-lowing) of independent auditors. Also, the results showed that auditors’ ethical style (honesty and correctness of the auditor, competence of the auditor, and impartiality of the auditor) has a positive effect on the disclosure (whistle-blowing) of independent auditors.

References

P. Alleyne, M. Hudaib, and R. Pike, "Towards a conceptual model of whistle-blowing intentions among external auditors," The British Accounting Review, vol. 45, no. 1, pp. 10-23, 2013/03/01/ 2013, doi: https://doi.org/10.1016/j.bar.2012.12.003.

G. Lee and X. Xiao, "Whistleblowing on accountingy-related misconduct: A synthesis of the literature," Journal of Accounting Literature, vol. 41, no. 1, pp. 22-46, 2018, doi: 10.1016/j.acclit.2018.03.003.

G. R. d. Silva and R. G. d. Sousa, "A influência do canal de denúncia anônima na detecção de fraudes contábeis em organizações," Revista de Contabilidade e Organizações, vol. 11, no. 30, pp. 46-56, 09/29 2017, doi: 10.11606/rco.v11i30.134372.

B. d. A. Guelber Fajardo and R. L. Cardoso, "Do as I Say, Don't Do as I Do: How Individual and Relational Characteristics Influence Whistleblowing," Contabilidade Gestão e Governança, vol. 17, no. 1, pp. 115-133, 2014.

R. A. D. Condé, "Fraudes corporativas: um estudo de casos múltiplos à luz da teoria dos escândalos corporativos," Universidade do Estado do Rio de Janeiro, 2013. [Online]. Available: http://www.bdtd.uerj.br/handle/1/8091

A. Fonseca, "Brasileiros tendem a aceitar ações antiéticas," Valor Econômico, 2020.

S. E. Kaplan and S. M. Whitecotton, "An Examination of Auditors' Reporting Intentions When Another Auditor Is Offered Client Employment," AUDITING: A Journal of Practice & Theory, vol. 20, no. 1, pp. 45-63, 2001, doi: 10.2308/aud.2001.20.1.45.

M. B. Curtis and E. Z. Taylor, "Whistleblowing in public accounting: Influence of identity disclosure, situational context, and personal characteristics," Accounting and the Public Interest, vol. 9, no. 1, pp. 191-220, 2009.

T. M. Tuan Mansor, A. Mohamad Ariff, and H. A. Hashim, "Whistleblowing by auditors: the role of professional commitment and independence commitment," Managerial Auditing Journal, vol. 35, no. 8, pp. 1033-1055, 2020, doi: 10.1108/MAJ-11-2019-2484.

D. L. Seifert, J. T. Sweeney, J. Joireman, and J. M. Thornton, "The influence of organizational justice on accountant whistleblowing," Accounting, Organizations and Society, vol. 35, no. 7, pp. 707-717, 2010.

L. M. D. Maragno and N. Cordeiro, "The influence of locus of commitment and ethical style on independent auditors’ whistleblowing," Revista de Contabilidade e Organizações, vol. 16, 2022, doi: https://doi.org/10.11606/issn.1982-6486.rco.2022.185317.

E. Z. Taylor and M. B. Curtis, "An examination of the layers of workplace influences in ethical judgments: Whistleblowing likelihood and perseverance in public accounting," Journal of Business Ethics, vol. 93, pp. 21-37, 2010.

J. R. Mesmer-Magnus and C. Viswesvaran, "Whistleblowing in organizations: An examination of correlates of whistleblowing intentions, actions, and retaliation," Journal of business ethics, vol. 62, pp. 277-297, 2005.

R. K. Chiu, "Ethical judgment and whistleblowing intention: Examining the moderating role of locus of control," Journal of business ethics, vol. 43, pp. 65-74, 2003.

T. I. White, Discovering philosophy. Hackett Publishing, 2022.

D. B. D. Sampaio and F. Sobral, "Speak now or forever hold your peace?: An essay on whistleblowing and its interfaces with the Brazilian culture," BAR-Brazilian Administration Review, vol. 10, pp. 370-388, 2013.

J. P. Near and M. P. Miceli, "Organizational dissidence: The case of whistle-blowing," Journal of business ethics, vol. 4, pp. 1-16, 1985.

J. Rothschild, "The Fate of Whistleblowers in Nonprofit Organizations," Nonprofit and Voluntary Sector Quarterly, vol. 42, no. 5, pp. 886-901, 2013/10/01 2013, doi: 10.1177/0899764012472400.

M. P. Miceli, J. P. Near, M. T. Rehg, and J. R. Van Scotter, "Predicting employee reactions to perceived organizational wrongdoing: Demoralization, justice, proactive personality, and whistle-blowing," Human relations, vol. 65, no. 8, pp. 923-954, 2012.

S. Valentine and L. Godkin, "Moral intensity, ethical decision making, and whistleblowing intention," Journal of Business Research, vol. 98, pp. 277-288, 2019/05/01/ 2019, doi: https://doi.org/10.1016/j.jbusres.2019.01.009.

C. Willett and M. Page, "A Survey Of Time Budget Pressure And Irregular Auditing Practices Among Newly Qualified Uk Chartered Accountants," The British Accounting Review, vol. 28, no. 2, pp. 101-120, 1996/06/01/ 1996, doi: https://doi.org/10.1006/bare.1996.0009.

D. Dalton and R. R. Radtke, "The joint effects of Machiavellianism and ethical environment on whistle-blowing," Journal of business ethics, vol. 117, pp. 153-172, 2013.

M. B. Curtis, "Are audit-related ethical decisions dependent upon mood?," Journal of business ethics, vol. 68, pp. 191-209, 2006.

H. Park and J. Blenkinsopp, "Whistleblowing as planned behavior–A survey of South Korean police officers," Journal of business ethics, vol. 85, pp. 545-556, 2009.

R. L. Sims and J. P. Keenan, "Predictors of external whistleblowing: Organizational and intrapersonal variables," Journal of business ethics, vol. 17, pp. 411-421, 1998.

H. Park, M. T. Rehg, and D. Lee, "The influence of Confucian ethics and collectivism on whistleblowing intentions: A study of South Korean public employees," Journal of Business Ethics, vol. 58, pp. 387-403, 2005.

B. R. MacNab and R. Worthley, "Self-efficacy as an intrapersonal predictor for internal whistleblowing: A US and Canada examination," Journal of Business Ethics, vol. 79, pp. 407-421, 2008.

E. Shepherd, A. Stevenson, and A. Flinn, "Information governance, records management, and freedom of information: A study of local government authorities in England," Government Information Quarterly, vol. 27, no. 4, pp. 337-345, 2010/10/01/ 2010, doi: https://doi.org/10.1016/j.giq.2010.02.008.

T. Barnett, "A preliminary investigation of the relationship between selected organizational characteristics and external whistleblowing by employees," Journal of business Ethics, vol. 11, pp. 949-959, 1992.

S. N. Robinson, J. C. Robertson, and M. B. Curtis, "The effects of contextual and wrongdoing attributes on organizational employees’ whistleblowing intentions following fraud," Journal of business ethics, vol. 106, pp. 213-227, 2012.

V. Morás, T. de Souza, and P. da Cunha, "Ameaças à independência do auditor: uma análise a partir da percepção de auditores independentes em consonância a NBC PA 290," Contabilidade Vista & Revista, vol. 30, no. 3, pp. 46-72, 2019.

P. Alleyne, R. Haniffa, and M. Hudaib, "Does group cohesion moderate auditors’ whistleblowing intentions?," Journal of International Accounting, Auditing and Taxation, vol. 34, pp. 69-90, 2019.

N. U. Prasetyaningsih, "The role of moral reasoning on the effects of incentive schemes and working relationships on whistleblowing: An audit experimental study," (in English), Gadjah Mada International Journal of Business, Journal Article vol. 23, no. 3, pp. 215-236, 2021, doi: https://search.informit.org/doi/10.3316/informit.147474299944971.

H. Varasteh, H. Nikoomaram, and A. Jahanshad, "auditors desire to whistleblowing Based on social cognition theory," Audit Science, vol. 21, no. 82, pp. 89-110, 2021.

S. Dammak, S. Mbarek, and M. Jmal, "The Machiavellianism of Tunisian accountants and whistleblowing of fraudulent acts," Journal of Financial Reporting and Accounting, vol. ahead-of-print, no. ahead-of-print, 2022, doi: 10.1108/JFRA-09-2021-0296.

N. Iqbalifar, G. a. Talibnia, and H. Vakilifard, "The effect of the organization's ethical due diligence tools on the warning of financial corruption in audit institutions," (in fa), Ethical research, vol. 41, no. 11, pp. 47-70, 2020. [Online]. Available: https://www.noormags.ir/view/en/articlepage/1684143.

M. goldoost, G. Talebnia, A. Esmaelzadeh mogharri, F. Rahnamaye roodposhti, and R. royaee, "Analysis of the Relationship between Ethical Awareness and the Ethical Judgment of the Professionals in the public accounting profession to the Whistle-blowing of Financial Violations (Case Study of Guilan Province)," Governmental Accounting, vol. 5, no. 1, pp. 85-98, 2019, doi: 10.30473/gaa.2019.43719.1233.

B. Banimahd and A. Golmohamadi, "Investigating the relationship between ethical climate and Whistleblowing through optional reporting model in Iran's audit profession," (in eng), Iranian journal of Value & Behavioral Accounting, Research vol. 2, no. 3, pp. 61-86, 2017, doi: 10.29252/aapc.2.3.61.

Ali Mohammed Hassan AL-Bakate, Sohad Sabih Al-Saffar " The Relationship Between the Policies and Procedures of International Auditing Standard (220) Quality Control and Enhancement of Audits," Journal of Techniques, ISSN: 2708-8383, Vol. 4, No. 4, December 31, 2022, Pages 246-257.